Oil prices began climbing in January 2026 amid the escalating U.S. and Israeli confrontation with Iran, then spiked when war broke out on February 28 and Iran closed the Strait of Hormuz. Brent crude rose by roughly 70% within weeks. By June, a fragile ceasefire had brought prices part of the way back down. Whether the calm holds depends on further diplomatic negotiations between the warring parties. Whatever the negotiators do next, this shock continues to stress economies and food systems around the world, though effects vary by region and country. Has it reached (or will it reach) Africa’s food systems, and where?

Fuel is an integral element of modern food systems. Diesel powers the vast majority of trucks and vans that form the backbone of the transportation networks around the world that move food from rural producers to urban consumers and elsewhere. By definition, the more processing, transport, and handling a food undergoes on its way to consumers, the larger its post-farmgate value chain, and the more stages at which fuel costs can enter.

That dependence is especially acute in Africa, where many countries are vast and landlocked, and food typically travels long overland distances by road. Traveling from farms to distant ports or interior markets often involves journeys of hundreds or kilometers and sometimes far more, building the price of diesel deep into the price of food. For example, in East African markets, oil price shocks raise domestic diesel prices that in turn increase local staple prices—independent of global grain prices or the exchange rate.

Yet an analysis across dozens of African countries shows that in the case of the Iran war, the same shock has produced sharply different outcomes for domestic fuel and food markets. The striking conclusion is how little the global price alone explains. Rather, prices are governed less by global markets and supply disruptions than by domestic fuel pricing and the fiscal structures that govern them.

The average is misleading

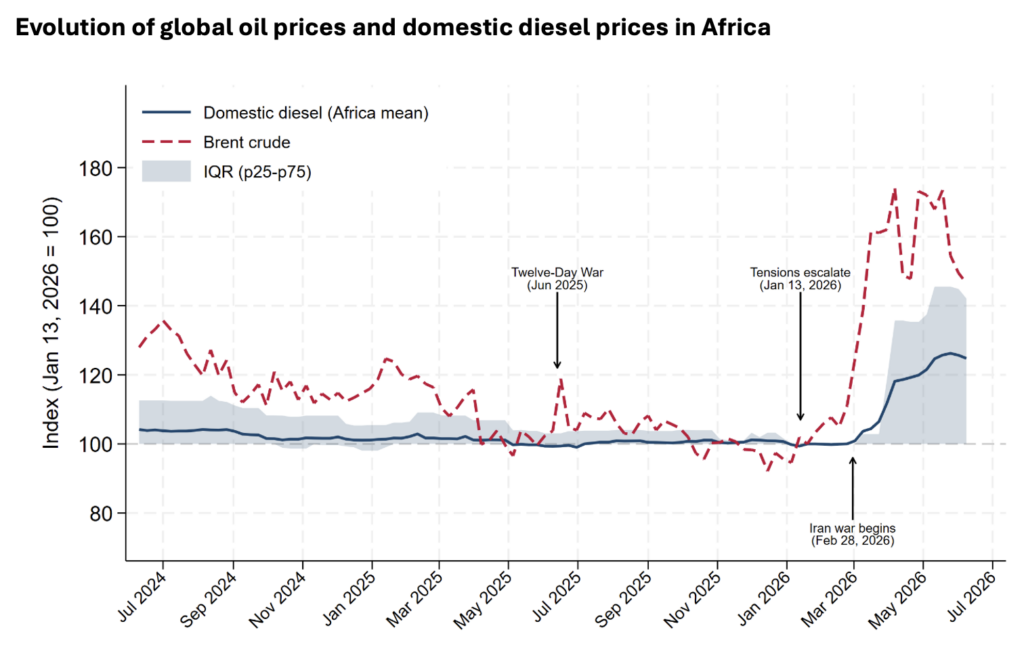

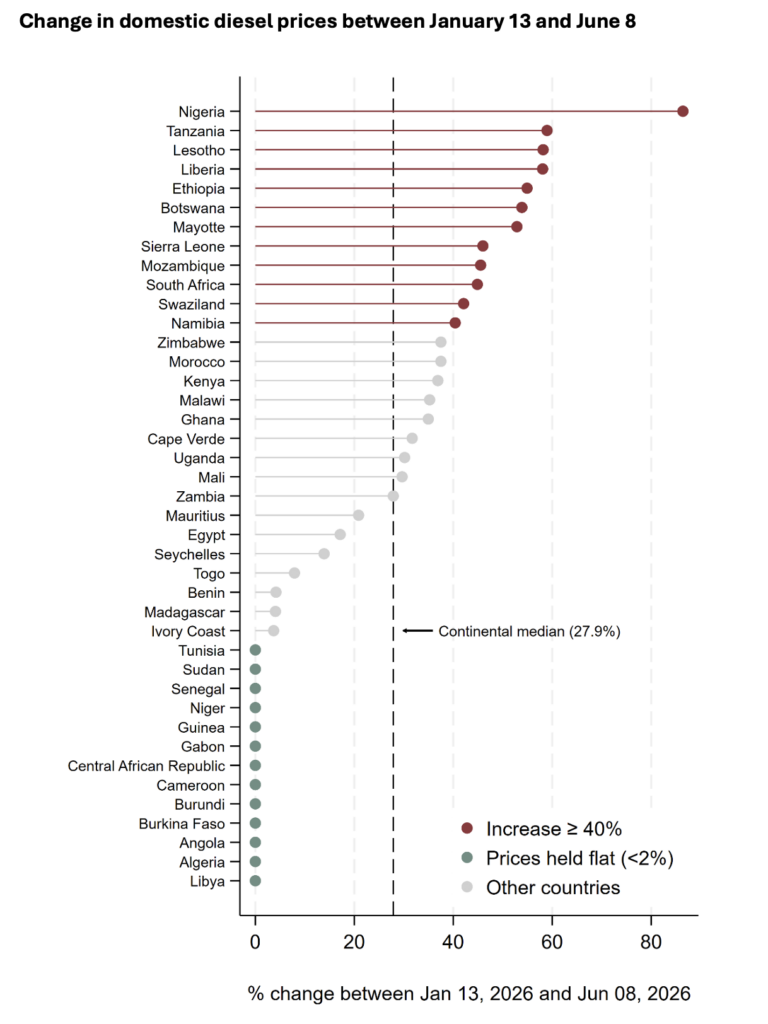

Between mid-January and mid-June, the average domestic diesel price across Africa rose far less than that of global crude, around 25% vs. 70% (Figure 1). Yet that average obscures enormous heterogeneity (Figure 2). During the same period, the change in domestic diesel prices ranged from essentially zero in a dozen countries (Algeria, Angola, Burkina Faso, Cameroon, Niger, Sudan, and others held prices flat) to increases of over 40% elsewhere. Nigeria sat at the top, with diesel up 86% in local-currency terms; Tanzania, Ethiopia, Lesotho, and Liberia saw well above 50% increases.

In other words, there was no single “African” experience of the 2026 oil shock. There were 42 distinct experiences across the 42 countries for which we have diesel price data. These patterns challenge conventional interpretations and responses, which usually assume similar transmission channels and integration (pass-through) between global and domestic markets.

Figure 1

Notes: All prices indexed to week of January 13, 2026; vertical axis measures price changes in percentages relative to that date. IQR = Interquartile range; the difference between the first quartile (or 25th percentile) and the third quartile (75th percentile).

Figure 2

It’s the structures, not the shock

In Nigeria, where diesel prices are now largely market-determined and broader petroleum-product subsidies have been unwound since 2023, the global shock transmitted rapidly to domestic pump prices. In much of francophone West and Central Africa, where the CFA-franc countries run a shared administered pricing framework insulated from currency risk by the euro peg, pump prices barely moved.

The implication is that the latter countries absorbed the difference onto their own balance sheets. Malawi provides another, cautionary, tale: large diesel price increases in October 2025 and January 2026—cumulatively totaling nearly 89%—preceded the Hormuz shock entirely, reflecting a domestic correction that brought pump prices in line with the market rate as part of exchange rate unification. Diesel rose further in April, tracking rising international prices, but within that same framework. The Malawi case is therefore less a story of crude-price transmission than of a domestic pricing regime catching up with itself, with the oil shock arriving on top of an already unsettled baseline.

The dispersion in diesel prices in these and other examples thus measures effects of the structures that translate global prices into domestic ones: whether fuel is administered or market-priced, how much fiscal space a government has, the state of foreign-exchange reserves, and whether a country exports or imports oil.

Holding prices flat while crude rises is an active, costly choice, typically financed through direct subsidies or tax cuts. Many governments have tried to hold off the pass-through from global oil markets to domestic fuel pumps: a World Bank tracker records dampening measures in most countries with data.

However, many African countries that took such measures saw diesel prices rise sharply anyway, because the subsidy was too small or the fiscal capacity ran out. Who can sustain these measures? There is no simple answer. Several of the countries still holding diesel prices flat are among those projected to be most fiscally vulnerable to the crisis, Burkina Faso among them, given high import dependence and thin reserves—so for them the fiscal reckoning will likely be deferred rather than avoided. The same logic extends to food prices directly: Egypt’s long-standing wheat subsidy may insulate consumers from global price shocks, but at an ongoing fiscal cost.

Food prices: Quiet so far—but the test hasn’t arrived

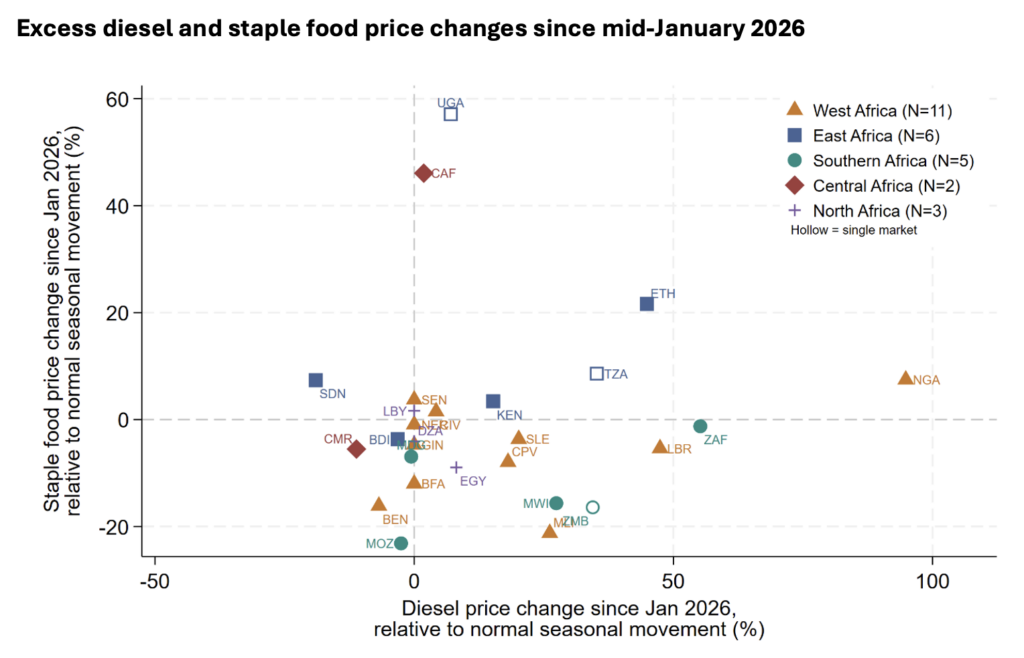

If diesel prices rose 40% or more in some countries, how would food prices be affected? Measuring this is not straightforward, as food price data across Africa vary in coverage and frequency. To address this question, we focused on each country’s dominant staple, held the reporting markets constant over time, matched the diesel and food time periods, and expressed both relative to normal seasonal movement. The result is a matched diesel-and-staple price series for 27 countries, some of which rest on a single food market (Figure 3).

Thus far, food prices appear stable. Across the range of diesel increases, staple prices show no systematic above-normal movement. Nigeria’s diesel rose most of all, yet the sorghum series used here sits only marginally above its seasonal norm. This should not be read as an absence of food price stress, but rather as evidence that the additional fuel price shock had not yet clearly appeared in this particular staple-price series. South Africa and Liberia saw large diesel increases and flat-to-negative staple prices. Kenya, with the deepest food price market coverage, shows essentially no change.

Official consumer price indices (CPIs, which capture the representative consumer basket, not a single commodity) tell a consistent story: across 18 African countries where food and transport prices are tracked separately, transport prices since January have risen an average of 6 percentage points above their prior-year norm, while food prices have edged up only about 1 percentage point above normal (authors’ calculations from IMF CPI data). Nigeria, where diesel rose most, offers an early signal of the food channel activating: year-on-year food inflation nearly doubled between January and May 2026 (from 9% to 17%), even as inflation excluding food and energy continued to fall.

Why flat food prices may not last

The picture of flat food prices across Africa is easy to misread as reassurance, for two independent reasons.

The first is timing. The oil-to-food channel is real and, by one careful estimate, fast relative to other price shocks. Dillon and Barrett (2016) find that in East African markets, a global oil price shock reaches local maize prices more quickly than a global maize price shock does. The effect is also sizable: a 1% rise in oil lifts local maize by about 0.26%, even holding global grain prices and the exchange rate fixed. Applied mechanically to a 70% crude spike, that elasticity would imply an eventual maize price increase on the order of 18%, had the full chain run as it did in their sample.

The same study finds that completing 80% of the pass-through from global oil to local maize takes around nine months on average across their markets. The food price data end in May, three months after the war began and the Brent crude price surged in late February—and far earlier than the nine-month average time to pass-through, or even to the fastest interior market in their sample (~7 months).

The second reason is that the chain runs in two steps: from global oil to domestic diesel, then from diesel to food. In the dozen countries that held diesel flat (Figure 2), the first step never happened, so there is nothing to pass on to food prices. Where it did reach the pump—Nigeria above all, where diesel rose 86% in local-currency terms, reflecting a combination of global prices, exchange-rate depreciation, and import-parity dynamics—the second step is simply slow, so little impact should have surfaced yet.

Where the second step is still to come, when it arrives matters. If it lands in the lean season —when food stocks are down and rural incomes at their annual low—the same price increase does more damage, because it hits when households can least absorb it. The markets to watch are those where domestic diesel prices rose sharply and the lean season is approaching. Since that season arrives at different times across the continent, they will not all come due at once.

Figure 3

Note: Each point is a country, N = 27. “Excess” change is the 2026 percentage change minus the mean percentage change over the same calendar window in 2022–2025. Diesel window matched to each country’s food price endpoint. Food prices refer to the dominant staple: maize in eastern and southern Africa, millet in the Sahel, rice in coastal West Africa, sorghum for Nigeria and Sudan, and wheat for Algeria, Egypt, and Libya. Dashed lines at zero indicate no deviation from normal seasonal movement. Hollow markers (Uganda, Tanzania, and Zambia) are based on only one food market and therefore warrant caution.

Reducing exposure, not just absorbing shocks

Most African countries depend on imported fuel, which leaves them exposed to shocks they cannot control. The same chokepoints carry imported fertilizer, compounding the dependence. A few countries are starting to address their vulnerability and exposure directly rather than just cushioning its effects. Ethiopia has invested heavily in renewable energy, banned imports of combustion-engine vehicles in favor of electric ones, and signed an agreement to build a domestic urea complex—all aimed at reducing the country’s reliance on global supply chains. In Nigeria, investments in domestic refining capacity and fertilizer production are reducing reliance on import logistics and foreign-exchange constraints.

Not every country can follow these examples. But leaving the structures that determined who felt this shock in place would mean the same ones will determine who feels the next. In a world of increasing volatility, resilience may ultimately mean reducing exposure to shocks, not just finding ever-costlier ways to absorb them.

Kalle Hirvonen is a Senior Research Fellow with IFPRI’s Poverty, Gender, and Inclusion (PGI) Unit; Katrina Kosec is a PGI Senior Research Fellow; Kibrom Abay is a Senior Research Fellow with IFPRI’s Development Strategies and Governance Unit. Opinions are the authors’.

This work was undertaken as part of the CGIAR Science Programs on Food Frontiers and Security and Policy Innovations. The authors thank all funders who supported this research through their contributions to the CGIAR Trust Fund.