Key takeaways

- India’s economy is highly exposed to fuel and fertilizer supply disruptions from the closure of the Strait of Hormuz, an economic modeling analysis shows.

- GDP and household incomes fall across all modeled scenarios. Higher input costs and supply disruptions hit farmers hardest and slow overall economic growth.

- Technology offers the most effective policy path to cushion the blow and build resilience. Improving fertilizer efficiency can limit losses while avoiding large subsidy-driven fiscal pressures.

The closure of the Strait of Hormuz has increased the cost of natural gas, disrupted supplies of key fertilizers, and increased cultivation costs around the world—ultimately affecting both farmers’ incomes and household food bills. For India, it is a reminder that the reliability of food systems depends not only on farm-level production, but also on the stability of energy supplies, shipping routes, and agri-input markets. This is because India’s fertilizer security is deeply tied to global supply chains. The country imports a significant share (~60%) of its diammonium phosphate (DAP) fertilizer, remains fully dependent on imported potash, and even domestic urea production relies heavily on imported liquefied natural gas (LNG). Nearly 50% of India’s LNG and about 85% of its crude oil requirements are also met through imports.

Global crude oil and fertilizer prices shot up by 58% and 66%, respectively, from February (pre-conflict) to April 2026, according to World Bank data. (More recently, those prices have fallen as Iran and the United States pursue negotiations, though shipping through the strait remains uncertain.)

Prices still face extreme upside risks if the geopolitical situation in the region worsens. On the assumption that the conflict ended in April 2026, the International Monetary Fund (IMF) forecasts the average price of crude oil to increase from $69 per barrel in 2025 to $82/bbl in 2026. However, if the war continues up to July 2026, the average price of crude oil is expected to be around $100/bbl in 2026 and might rise further to $125/bbl if the war persists until the end of 2026. In addition to the price spikes, the Indian fertilizer sectors will witness a severe shortage of raw materials due to the halt of shipments through the Strait of Hormuz.

In this post, we assess the short-run effects of such global commodity price shocks on India’s economy and discuss their potential implications for the country’s fertilizer policies. We employed IFPRI’s Rural Investment and Policy Analysis (RIAPA) model to estimate the Iran war’s impact on key macroeconomic indicators such as GDP, exports, imports, and the government budget deficit, and household income. The results show broad negative effects, with falling GDP and incomes of both farm and non-farm households. They also suggest the optimal solution is broad upscaling of technologies to minimize fertilizer usage.

Model details

The model was calibrated using a 2022-23 Social Accounting Matrix (SAM) of India. Specifically, the following scenarios were explored:

1. Full pass-through, where the government allows the domestic prices of fertilizers to move in tandem with those in the international market.

2. Absorption, where the government protects its citizens by fixing domestic fertilizer prices at their pre-crisis levels.

3. Technology adoption, where the focus is on upscaling fertilizer savings technology to improve efficiency in chemical fertilizer use. Here we have considered a 5% reduction in chemical fertilizer intensity through upscaling of nutrient management technologies across Indian states.

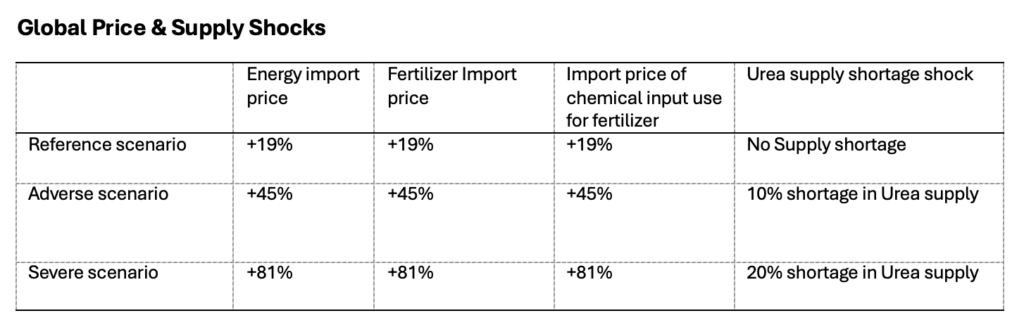

All these scenarios were considered under three different international price scenarios: Reference (conflict ceases, and prices stabilize from April 2026), Adverse (conflict lasts till June 2026), and Severe (conflict continues through the end of 2026). Table 1 provides details about the assumptions for fertilizer and petroleum prices in each scenario.

Table 1

Note: IMF’s assumptions for Crude oil price trend are assumed for fertilizer and chemical input price

Impacts on GDP and household incomes

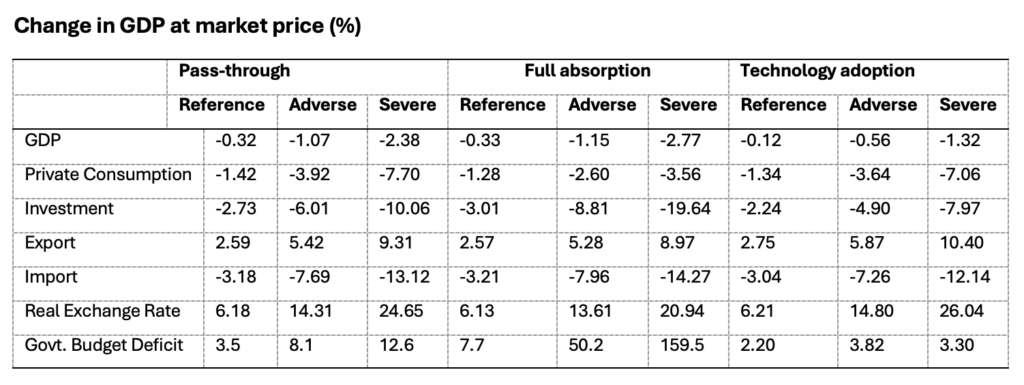

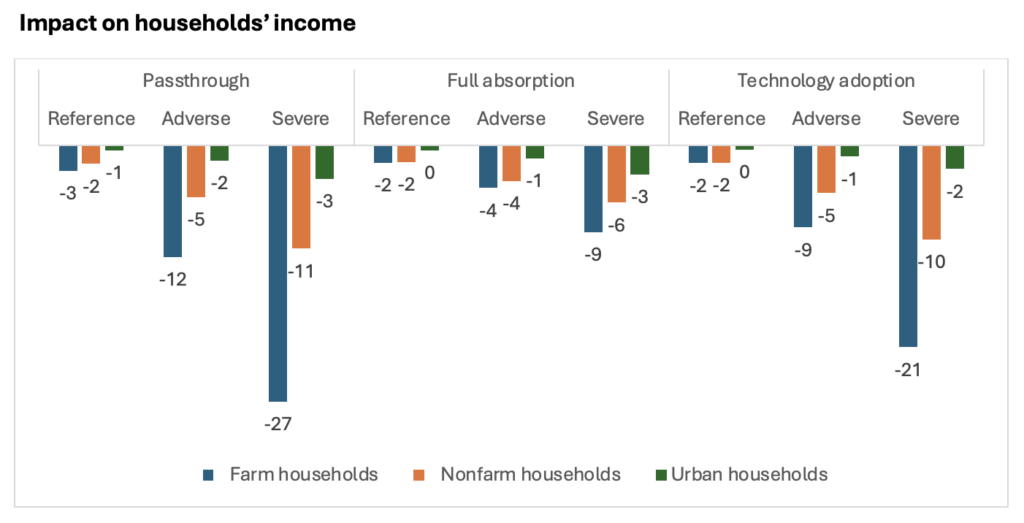

Results (Table 2 and Figure 1) reveal that under the full pass-through scenario with the conflict ending in April (Reference price scenario), India’s GDP falls by 0.32% and the incomes of the agricultural households fall by 2.6%. But with a longer conflict and sustained supply disruptions and high prices, the impacts worsen considerably. In the case of the Adverse price scenario, there is significant macroeconomic harm, with India’s GDP declining by 1.07% and the incomes of the farming households reduced by 11.65%. Under the Severe scenario, GDP falls by 2.38% and farming household income by 27%.

Incomes of rural non-farming households decline by 1.9%, 5.39%, and 10.77% under the Reference, Adverse, and Severe scenarios, respectively, while urban households record smaller income declines of 0.51%, 1.56%, and 3.47%.

The greater declines associated with the longer scenarios reflect probable worsening price and production conditions within India. The simultaneous effects of increasing costs and declining fertilizer production due to global supply disruptions shift the crisis from a quick shock to a longer, more uncertain period of sustained economic harm.

Table 2

Across all price scenarios, the main factors responsible for falling GDP are the decline in private consumption expenditures and the reduction in investments (Table 2). Rising global import prices lead to increased demand for foreign currency to pay for the imported goods. The national currency weakens and domestic prices rise.

Under the pass-through scenario, with rising global prices passed on to users but subsidies increasing proportionally to price, the government budget deficit rises by 3.5%, 8.1%, and 12.6% under the reference, adverse, and severe scenarios, respectively (Table 2).

However, the deficit balloons under the full absorption scenario (as the government fully subsidizes higher fertilizer costs to freeze fertilizer prices at the pre-conflict level), expanding by 7.7%, 50.2%, and 159.5% under the three price scenarios.

A large increase in the budget deficit is likely to lead to significant spending cutbacks and eventually to reduced investments in the economy.

Exports are one potential bright spot. Currency depreciation makes it cheaper for India to export goods to other countries—an important benefit in every scenario (Table 2). However, export growth does not prevent a drop in GDP. This is because impacts of the crisis fall heavily on private consumption, which accounts for about 65% of India’s GDP, according to government statistics. Even a smaller contraction in private consumption than those modeled will severely and adversely impact overall GDP.

Figure 1

Subsidies and budget deficits

The analysis suggests there is an important trade-off between fully protecting farmers from price shocks and sustaining GDP growth.

In the case of the Adverse price path, the full absorption scenario (in which subsidies fully cover price increases, protecting farm income) leads to higher overall losses of GDP: 1.15% compared to 1.07% in the case of full pass-through (Table 2). In the Severe price path, this structural disparity intensifies: absorption results in a 2.77% GDP decline compared to 2.38% for full pass-through (Table 2).

Yet the results also show that when the government fully absorbs price increases, there are clear benefits for farmers. Under the Adverse price path, farm household incomes fall by only 4.4% if absorption is complete but by 11.6% under the pass-through scenario (Figure 1).

Fully insulating farmers from high prices requires an aggressive increase in the budget for fertilizer subsidies. The model shows that such increases lead to a widening of the public budget deficit and hence crowding out of public capital spending—hurting GDP.

The key role of technology to reduce fertilizer intensity

Thus, while fiscal policy intervention is an important tool for short-run income support for poor farmers, the cost to fixed investment is bound to have severe consequences. This indicates that upscaling technology to reduce fertilizer intensity can be an option to make long term economic growth sustainable. This includes programs focused on better targeting application, improving soil health, water management, and crop varieties, and other approaches.

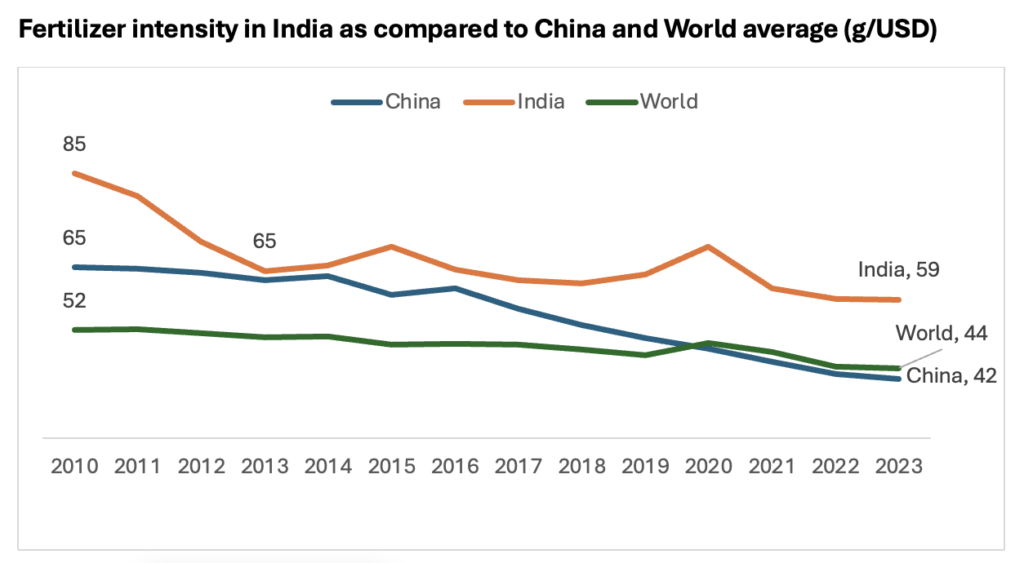

India’s fertilizer intensity remains higher than both China’s intensity and the world average (Figure 2). While both China and India substantially reduced intensity between 2010 and 2023, India’s reduction was only significant between 2010 and 2013, slowing down considerably between 2013 and 2023 due to the government’s fertilizer subsidy policy, aimed at supporting increased application but not efficiency. Despite these differing trajectories in fertilizer intensity, both China and India experienced an average 4% growth in agricultural gross value added (GVA) between 2010 and 2023.1

India’s higher fertilizer intensity relative to China and the world average clearly highlights the significant potential for further efficiency gains without compromising agricultural output growth. That requires scaling up fertilizer-saving technologies across India.

For illustration purposes, this study assumes a 5% improvement in fertilizer intensity to analyze its impact on key macroeconomic indicators. As shown in Table 2, adopting fertilizer-saving technology under the Adverse price scenario limits India’s GDP loss to 0.56%, compared to a 1.07% loss under the same scenario without technology adoption. Furthermore, with technology adoption, farm households face a 9% income loss under the adverse scenario, compared to a 12% loss without it. This implies that even a modest 5% improvement in fertilizer efficiency can partly mitigate losses to both national GDP and household income.

However, even under this optimistic scenario of a 5% improvement, it will still take six to seven years to match China’s current levels of fertilizer intensity.

Figure 2

Note: Fertilizer intensity is measured as grams of nutrient (Nitrogen + Phosphate + Potash) per dollar value of agricultural produce

Policy implications

These findings clearly demonstrate that India’s fertilizer policy must shift from short-term price management to long-term risk management. While price management shields farmers post-shock, risk management policies such as improving fertilizer intensity build proactive, long-lasting resilience against external disruptions.

Because fertilizers link energy security, public finance, soil health, and food-price stability, disruptions in global energy markets or shipping routes quickly cascade into higher domestic cultivation costs and household inflation.

Managing this interconnected system requires comprehensive food systems governance. Relying solely on subsidy policy or incentive designs is insufficient. For instance, nearly three years after its approval, the Prime Minister Programme for Restoration, Awareness Generation, Nourishment, and Amelioration of Mother Earth (PM-PRANAM) scheme—which aims to promote sustainable fertilizer use—has disbursed no incentives to states. A successful nutrient transition requires reliable data, credible baselines, and viable alternatives so states and farmers can adopt balanced nutrient use without risking productivity.

Fertilizer use is shaped not only by subsidy policy but also by cropping patterns, procurement incentives, irrigation practices, energy prices, import strategy, soil-health information, climate goals, and farmer risk. The policy levers for these sit across different ministries and institutions, but their effects converge on the same farm. Without an institutional mechanism to connect them, India will continue to design input, energy, trade, soil health, and sustainability policies in separate silos.

A food systems governance approach would not replace existing ministries or schemes. Rather, it would align them around shared outcomes: stable food prices, lower input vulnerability, efficient nutrient use, improved soil health, fiscal sustainability, and climate resilience. It should also support an integrated fertilizer-risk monitoring system that links geopolitical risk, energy prices, shipping routes, domestic stocks, subsidy exposure, crop calendars, and state-level demand. The Iran war crisis shows why such coordination can no longer be just an academic idea. It is a practical requirement for managing risk in an interconnected food economy.

Our findings show that the Iran conflict’s impact on the Indian economy is likely to be significant—and that even if impacts are limited, the country remains exposed to global disruptions in fuel and fertilizer markets. The current moment thus offers an opportunity to policymakers to build long-term resilience—if they are ready to take it.

Barun Deb Pal is a Research Coordinator with IFPRI’s Foresight and Policy Modeling Unit; Anjani Kumar is a Senior Research Fellow with IFPRI’s Development Strategies and Governance (DSG) Unit. Smita Sirohi is Indian Council of Agricultural Research (ICAR) National Professor, MS Swaminathan Chair; Banda Sainath is a Scientist with ICAR; Kriti Sharma is a DSG Research Analyst; Praveen K.V. is a Senior Scientist with ICAR. Authors are based in New Delhi.

This work was supported by the CGIAR Programs on Policy Innovations and Food Frontiers and Security and the Indian Council of Agricultural Research, Government of India. Opinions are the authors’.

1. FAOSTAT Data extracted on June 16, 2026, https://www.fao.org/faostat/en/#data/MK